Buying a home in Portugal is one of those ideas that feels wonderfully simple on the surface. An apartment in Lisbon. A quiet stone house in the countryside. A villa near the sea. For many people, it’s tied up with lifestyle dreams, retirement plans, or the idea of putting down roots in Europe.

And in fairness — buying property in Portugal is absolutely achievable for foreign buyers. There are no restrictions on foreign ownership. The legal system is well established. Transactions are enforceable. And thousands of expats successfully buy homes here every year.

But the process works very differently from the UK, US, or most of Northern Europe.

There is no MLS system. No escrow service. No title insurance industry. No standardised seller disclosures. And notaries, agents, and lawyers all play roles that don’t map neatly onto Anglo-American expectations.

Instead, Portugal operates on a mixture of formal law and informal practice. The law is clear and rigid. The day-to-day process is more flexible, relationship-driven, and occasionally opaque. That combination is where foreign buyers either sail through — or get caught out.

The goal of this guide is simple:

To explain how buying property in Portugal really works, in the order it actually happens, and to highlight the quiet little realities that estate agents’ glossy brochures tend not to mention.

We’ll cover:

- The step-by-step legal process, from offer to final deed

- The documents that define whether a property is truly “clean”

- Why deposits in Portugal carry more risk than most buyers expect

- How mortgages and bank valuations really work

- Common structural and licensing issues

- The quirks of listings, agents, and negotiation

- And the practical bureaucracy that begins after you get the keys

This isn’t a sales pitch. It’s the guide we wish every foreign buyer read before wiring a deposit.

If you understand how the system works before you start, buying in Portugal can be smooth, safe, and even enjoyable.

If you don’t — it can become expensive very quickly.

Let’s start at the beginning: how the Portuguese property search actually works.

I Want To Buy a Property in Portugal

The Portuguese Property Market in 2026: The Big Picture

Before getting into contracts and paperwork, it helps to understand the environment you’re stepping into.

Portugal’s property market in 2026 sits in an unusual place. Demand from foreign buyers remains high. Supply remains tight in many desirable areas. And prices, particularly in Lisbon, Porto, and much of the Algarve, have risen sharply over the past decade.

At the same time, Portuguese banks, regulators, and even the European Commission have repeatedly warned that property prices in Portugal are stretched relative to local incomes and rental yields. In practical terms, that means one thing for foreign buyers:

Market prices and bank valuations often live in different realities.

A seller may happily accept your €500,000 offer. But the bank’s appointed valuer may decide the same property is worth €420,000. If you’re relying on a mortgage, that gap becomes your problem — not the seller’s, and not the bank’s. This valuation gap is one of the most common reasons foreign purchases fall apart after a deposit has already been paid.

Another defining feature of the Portuguese market is the high proportion of cash buyers. Many local buyers sell an existing property before buying the next. Many foreign buyers arrive with capital released from higher-priced markets abroad. And some investors simply prefer to avoid Portuguese mortgage bureaucracy altogether.

Sellers know this. Which means:

- Cash buyers are often favoured

- Mortgage buyers need stronger contractual protection

- And speed and certainty frequently matter more than price

There’s also a structural transparency issue. Portugal has no public database of completed sale prices. Listing portals only show asking prices. Agents hold most transaction data privately. That makes it harder for buyers to know what a property is truly worth — and easier for asking prices to drift above fundamentals.

None of this means buying in Portugal is unsafe. But it does mean you’re entering a market where:

- Asking prices are often aspirational

- Bank valuations are conservative

- And due diligence sits almost entirely with the buyer

Understanding this context early makes the rest of the process much easier to navigate.

Next, we’ll look at how the Portuguese property search actually works — and why finding the right property is often harder than it looks online.

Finding a Property: What the Search Phase Really Looks Like

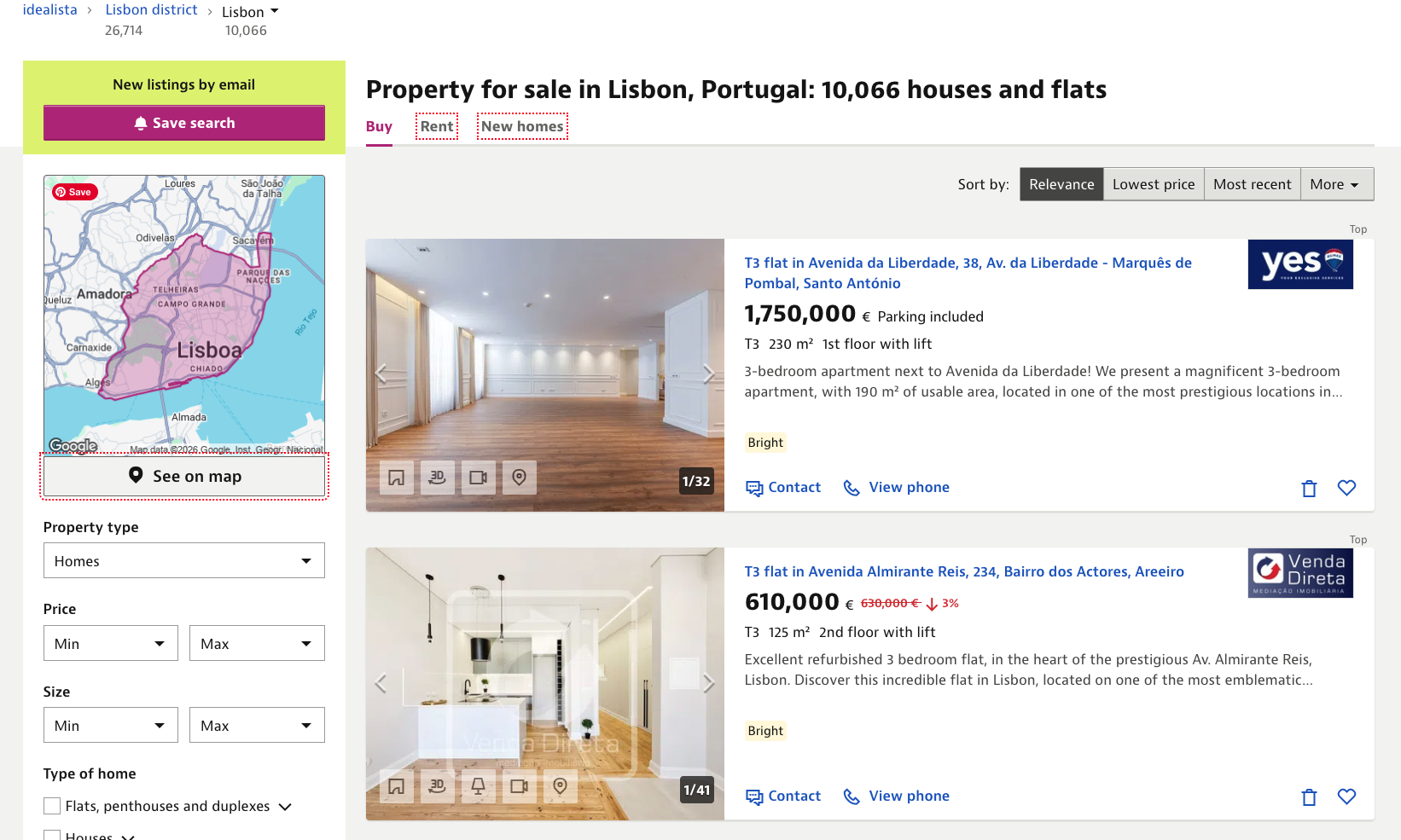

Most foreign buyers begin their search the same way: typing a budget into Idealista, Imovirtual, or Casa Sapo and scrolling through glossy photos of tiled terraces and ocean views.

These portals are useful. But they don’t work the way many buyers expect.

Portugal doesn’t have a centralised Multiple Listing Service (MLS). There’s no single authoritative database of properties for sale. Instead, each agency uploads its own listings — often without exclusivity. That creates a search environment that is more fragmented, less transparent, and more repetitive than buyers from the UK or US are used to.

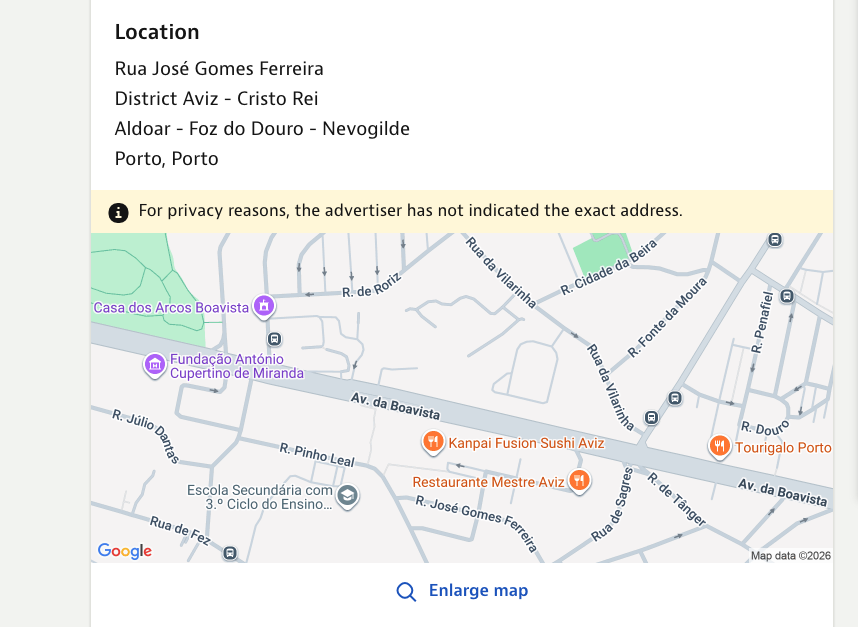

Why addresses are usually hidden

If you click on a listing in Portugal, you’ll usually see only a vague location — a parish name, neighbourhood, or approximate map pin. The exact street address is almost always missing.

This isn’t a technical limitation. It’s deliberate.

Agencies hide addresses to prevent competing agents from identifying the property and contacting the owner directly. It also prevents buyers from bypassing the agent and knocking on the seller’s door themselves.

For buyers, the practical consequence is simple:

You often can’t properly research a property — or even check the street — until you’ve contacted an agent and requested more details.

This is normal in Portugal. But it does mean:

- You’ll send more enquiries than you expect

- You’ll need to ask direct questions early

- And you’ll do more of your research after making contact, not before

Duplicate listings are standard

Because many properties are listed non-exclusively, it’s common to see the same house listed multiple times by different agencies. Sometimes the price differs. Sometimes the description or photo set is different. Sometimes one listing is current and another is months out of date.

This can be confusing at first. But it’s simply how the market operates.

If you like a property, assume:

- It may be listed elsewhere

- Another agent may actually hold the keys

- And some listings may still be online long after the property is sold

Once you start viewing seriously, most buyers end up working primarily with one or two responsive agents to cut through this duplication.

The reality of “bait” listings

A quieter but real feature of the Portuguese market is the existence of “bait” listings. These are attractive properties listed at very good prices that either:

- Have already sold

- Were never truly available

- Or exist mainly to generate buyer enquiries

When you ask about them, the agent replies that the property has “just gone” — and then offers to show you alternatives.

This isn’t universal, and many agencies operate professionally. But it happens often enough that experienced buyers treat any unusually good listing with healthy scepticism until a viewing is confirmed.

WhatsApp is the real communication channel

Another cultural difference surprises many foreign buyers:

Most serious communication happens on WhatsApp.

Agents will:

- Send viewing confirmations

- Share location pins

- Negotiate offers

- Forward documents

- And follow up on next steps

…all via WhatsApp.

It feels informal if you’re used to email-heavy processes. But in Portugal it’s standard business practice. Fast, casual, and ubiquitous.

The only important rule:

If something matters legally or financially, ask for it again by email. WhatsApp is great for speed — but you want a paper trail when contracts and deposits are involved.

Negotiation expectations

Portugal is not a sealed-bid, above-asking market by default.

Many properties — particularly older homes, rural properties, and long-listed apartments — are priced optimistically. Offering 5–15% below asking is normal. In some cases, larger reductions are achievable if a property has sat unsold for a long time.

However, in high-demand urban areas or prime coastal zones, asking price (or even higher) can still happen — especially when cash buyers are involved.

The key point:

Asking price in Portugal is an invitation to negotiate, not a final statement of value.

The human element

Finally, it’s worth remembering that Portugal remains a relationship-driven market.

Agents talk to each other. Sellers ask who you are. Local reputation matters. And sometimes a seller will choose a buyer they like over a slightly higher offer.

Being polite, patient, and clear goes a surprisingly long way.

Once you’ve found a property and agreed a price, the real legal process begins. And this is where Portugal diverges most sharply from Anglo-American expectations.

Next, we’ll look at what actually happens when you make an offer — and why reservation agreements and deposits work very differently here.

Making an Offer: From Handshake to Reservation

Once you’ve found a property you like, the next step is to make an offer. In Portugal, this part of the process is less formalised than in the UK or US — at least at first.

Most offers begin verbally. You tell the agent your proposed price and conditions. The agent takes it to the seller. There may be a bit of back-and-forth. When agreement is reached, everyone considers the property “agreed”.

But — and this is important — at this stage, nothing is legally binding.

Until a written contract exists, either side can still walk away without penalty. This is where many foreign buyers assume they’re further along than they really are.

Reservation agreements: optional, but common

To bridge the gap between verbal agreement and the full legal contract, many agencies introduce a reservation agreement.

This usually involves:

- A short document stating that the property is reserved for you

- A small payment, often €2,000–€10,000 (reserva)

- A reservation period of 15–30 days

- The promise that the property won’t be marketed during that time

On the surface, this feels like progress. In reality, reservation agreements in Portugal are lightly regulated and often poorly drafted.

Common problems include:

- Unclear refund conditions if legal issues appear

- No link to the later CPCV contract

- Money paid directly to the agent or seller

- No escrow or independent holding of funds

If the buyer later discovers a title problem, missing licence, or mortgage refusal, recovering a reservation fee can become difficult — especially if the agreement wording is vague.

When reservation agreements make sense

A reservation agreement can be useful if:

- Your lawyer has already reviewed the draft

- The money is held by your lawyer, not the agent

- The document clearly states full refund if due diligence fails

- The reservation period is short and defined

But many experienced buyers skip reservation agreements entirely and move straight to a properly drafted CPCV once due diligence begins.

The key principle

In Portugal, you don’t want to pay money to anyone until your lawyer is involved.

Not the agent.

Not the seller.

Not a “standard template” contract.

Once your offer is accepted, the next step should always be:

- Hire your lawyer

- Begin due diligence

- Draft the CPCV (promissory contract)

- Then pay the deposit under defined legal protection

Which brings us to the most important document in the entire Portuguese buying process.

Next, we’ll look at the CPCV — the promissory contract — and why deposits in Portugal carry much more risk than most foreign buyers expect.

The CPCV: The Contract That Locks Everything In

In most Anglo-American systems, the critical moment is “exchange of contracts”. In Portugal, that moment is the CPCV:

Contrato de Promessa de Compra e Venda

(Promissory Contract of Purchase and Sale)

Once the CPCV is signed, the deal is no longer casual. It is fully legally binding. And the financial consequences of getting it wrong are significant.

This is the point in the process where having your own independent lawyer stops being “nice to have” and becomes essential.

What the CPCV does

The CPCV sets out:

- The agreed purchase price

- The property identification and registry references

- The deposit amount (sinal)

- Deadlines for completion

- What fixtures and contents are included

- Conditions that must be met before completion

- Penalties if either side defaults

Once signed by both parties, the CPCV effectively “locks” the property off the market until the final deed is signed.

The deposit: the sinal

At CPCV stage, the buyer pays a deposit — typically:

- 10% of the purchase price

- Sometimes 20–30% for non-residents or high-demand areas

This is not a goodwill gesture. It is a statutory legal guarantee under Portuguese civil law.

The rule is simple:

- If the buyer defaults: the seller keeps the entire deposit

- If the seller defaults: the seller must return double the deposit

This rule applies automatically under Portuguese law, even if the contract wording is vague.

And crucially:

The deposit normally goes directly to the seller. Not escrow. Not the notary. Not a neutral account.

This is the single biggest shock for many foreign buyers.

Why this creates risk for foreign buyers

Once the CPCV is signed:

- If your mortgage is refused

- If the bank valuation comes in too low

- If you discover a legal or licensing issue too late

- If your funds transfer is delayed

- If you simply change your mind

You could lose the entire deposit.

There is no cooling-off period.

No automatic mortgage protection.

No “subject to survey” assumption unless you write it in.

This is why the CPCV must never be signed until due diligence has begun and financing strategy is clear.

The clauses that protect you

A well-drafted CPCV for a foreign buyer normally includes:

- Mortgage approval clause

Allowing withdrawal without penalty if financing is refused. - Bank valuation clause

Allowing withdrawal if the valuation is materially below purchase price. - Title and licensing clause

Making completion conditional on clean registry and valid habitation status. - Survey clause

Allowing renegotiation or withdrawal if serious structural defects appear. - Deadline flexibility

Allowing extension if bank or municipal delays occur.

These clauses are normal in foreign-buyer transactions — but they must be negotiated before signing. Sellers in hot markets may resist them. That’s a commercial decision — but you should always understand the risk you’re accepting if you proceed without them.

Registering the CPCV

There is also a little-known protection many buyers skip:

Your lawyer can register the CPCV at the Land Registry with “real effectiveness” (força registral). This means:

- The seller cannot secretly sell to someone else

- Your contractual right becomes visible on the property record

- Your position is protected against third-party claims

It costs a small fee — and is well worth doing on higher-value purchases.

The practical reality

Most smooth Portuguese property purchases follow this rhythm:

- Offer accepted

- Lawyer engaged

- Due diligence started

- CPCV drafted with protective clauses

- Deposit paid

- Mortgage finalised

- Deed signed

Most horror stories follow a different rhythm:

- Offer accepted

- Agent pushes for quick CPCV

- Deposit paid

- Problems discovered later

Understanding that difference is the single most important step in buying safely in Portugal.

Next, we’ll look at what happens after the CPCV — the mortgage process, bank valuations, and why financing in Portugal behaves very differently from the UK or US.

Mortgages and Bank Valuations: Where Many Deals Break

If you’re buying in cash, you can skip this section.

If you’re relying on a Portuguese mortgage — even partially — this may be the most important part of the entire guide.

Because in Portugal, the bank does not care what you agreed to pay.

The bank only cares what its own valuer says the property is worth.

And those two numbers often don’t match.

Pre-approval is not approval

Most buyers start by getting a mortgage pre-approval (pré-aprovação). This is useful, but limited. It confirms:

- Your income is acceptable

- Your documents are in order

- Your borrowing range is plausible

What it does not confirm is:

- That the bank will approve this specific property

- Or how much the bank will lend against it

Final approval only happens after:

- The CPCV is signed

- The bank instructs its own valuer

- The valuation report is delivered

Which means financing risk often sits after your deposit is already on the line — unless your CPCV protects you.

The valuation gap

Portuguese bank valuations are conservative by design.

Valuers typically use:

- Historical comparable sales

- Conservative square-meter metrics

- “Forced sale” style assumptions

This regularly produces valuations 10–20% below market purchase price — and sometimes more in overheated areas.

If you agreed to buy at €500,000

and the bank values at €420,000

the mortgage is based on €420,000, not €500,000.

If your LTV is 70%:

- Expected loan: €350,000

- Actual loan: €294,000

You must suddenly find €56,000 extra cash.

If you can’t — and your CPCV has no valuation clause — you could lose your deposit.

This scenario is not rare. It’s one of the most common failure points for foreign buyers.

Typical mortgage terms for foreign buyers

As of 2026, non-resident buyers (people who don’t live in Portugal) generally see:

- Maximum LTV: 60–75%

- Loan term capped by age (typically ending by age 75)

- Interest rates: variable or fixed, often 3.5–6%

- Mandatory life insurance

- Mandatory building insurance

Mortgage approval timelines:

- 3–6 weeks in straightforward cases

- Longer if documents come from abroad

- Longer again in August or holiday periods

Banks also work almost entirely in Portuguese. Many foreign buyers use mortgage brokers to manage communication.

Banks still care about licences

Despite the 2024 Simplex law allowing sales without habitation licences, many banks still refuse to lend on:

- Properties without valid Licença de Utilização

- Properties with unlicensed extensions

- Properties with unresolved registry mismatches

So a property can now legally be sold — but not mortgageable.

If you sign a CPCV assuming the new law “solves” the licence issue, you may discover the bank disagrees.

The clause that saves deals

Well-advised buyers include two critical CPCV protections:

- Subject to mortgage approval

- Subject to valuation not below X

These clauses allow:

- Deposit refund

- Or renegotiation

- Or exit without penalty

Sellers sometimes resist them — especially in cash-heavy markets — but the risk trade-off should be understood clearly before signing.

The practical rhythm

A safe financing sequence looks like this:

- Mortgage pre-approval obtained

- Offer accepted

- Lawyer drafts CPCV with mortgage + valuation clauses

- CPCV signed

- Valuation ordered immediately

- Mortgage final approval obtained

- Deed scheduled

A risky sequence looks like:

- Offer accepted

- CPCV signed quickly

- Deposit paid

- Valuation comes in low

- Financing gap appears

- Deposit at risk

Understanding this distinction prevents most financing-related disasters.

Next, we move away from financing and into something even more fundamental:

Whether the property you’re buying is legally what it appears to be on the ground.

That starts with three documents — and in Portugal, they often don’t match.

The Three Documents That Must Match

In many countries, if a property is listed for sale, there’s an assumption that the basic legal status is already settled. In Portugal, that assumption can be dangerous.

A property here is defined by three separate official records, held by three different authorities. A property is only truly “clean” when all three match each other and match the physical reality on the ground.

Surprisingly often, they don’t.

This is the root cause of many post-purchase problems — and exactly why Portuguese property lawyers spend so much time on due diligence.

1) The Certidão Permanente

(Land Registry — Conservatória do Registo Predial)

This is the definitive ownership record.

It shows:

- Who legally owns the property

- How ownership was acquired

- Any mortgages registered against it

- Court claims or legal disputes

- Rights of way or third-party rights

If there is one document your lawyer will not skip, it’s this one.

Common real-world issues found here:

- Property still registered in a deceased owner’s name

- Multiple heirs listed, not all participating in the sale

- Old mortgages never formally discharged

- Boundary descriptions that don’t match reality

If the name on the Certidão Permanente does not exactly match the seller’s ID, the sale cannot safely proceed until resolved.

2) The Caderneta Predial

(Tax Registry — Finanças)

This is the tax record.

It contains:

- The official tax value (VPT)

- Property type (urban or rustic)

- Official size and layout description

- Taxpayer information

This is where creative “tax optimisation” sometimes appears.

Real examples lawyers see:

- A home described as a “storage building” to reduce IMI tax

- A villa listed as 120m² when it is physically 200m²

- A house shown as “urban” in one record but “rustic” in another

If the tax description doesn’t match the physical property, problems arise later with:

- Mortgage approvals

- Future renovations

- Resale

- Or even tax penalties

3) The Licença de Utilização

(Habitation Licence — Câmara Municipal)

This certifies that:

- The building was constructed according to approved plans

- It is authorised for residential use

Buildings constructed before 1951 are typically exempt — but they still require a formal exemption certificate.

Properties built or modified after that date should have a licence matching the current structure. Many don’t.

Common mismatches:

- Extra floors or rooms not in the approved plans

- Garages or annexes never licensed

- Enclosed terraces added later

- Pools without permits

Since the 2024 Simplex reforms, a property can be sold even without presenting this licence — but that does not make the building legally compliant. It simply shifts the risk to the buyer.

Why mismatches are so common

Portugal’s property system evolved over decades of:

- Informal construction

- Generational inheritance

- Paper records later digitised

- Municipal archives that don’t always align

The result: discrepancies are normal enough that lawyers assume they exist until proven otherwise.

What your lawyer actually does

Proper due diligence means your lawyer will:

- Pull the Certidão Permanente

- Pull the Caderneta Predial

- Request municipal building records

- Compare all three

- Compare them against the physical property

Only when all four align:

Land Registry

Tax Registry

Municipal Licence

Physical reality

…is the property considered legally “clean”.

The notary will not do this for you

This surprises many foreign buyers:

The notary only checks that:

- The seller and buyer are correctly identified

- Taxes are paid

- Documents exist

The notary does not verify that:

- The licence matches the building

- The tax record matches the house

- Extensions are legal

- Boundaries are correct

If you sign without a lawyer having done these checks, any problem discovered later becomes your responsibility.

The practical takeaway

In Portugal:

A beautiful house can exist physically.

A legal house exists only on paper.

You need both to match.

Next, we’ll look at one of the most misunderstood areas of Portuguese property law — habitation licences and the 2024 “Simplex” changes — and why they matter much more to buyers than sellers.

Habitation Licences and the 2024 Simplex Law: Legal to Sell ≠ Legal to Live In

Until very recently, one of the strongest safety rails in Portuguese property transactions was simple:

You could not complete a sale without presenting a valid Licença de Utilização (habitation licence) — or an official exemption certificate for pre-1951 buildings.

That changed in 2024.

The government introduced the Simplex Urbanístico reforms to speed up housing transactions and reduce bureaucracy. One of the headline changes was that a deed can now be signed even if the habitation licence is missing, provided the buyer explicitly accepts this.

On the surface, this sounds like progress.

In practice, it has shifted legal risk from the seller to the buyer.

What the habitation licence actually does

A Licença de Utilização confirms that:

- The building was constructed under approved plans

- Safety and structural standards were met

- The property is authorised for residential use

It is the document that turns a structure into a legally habitable dwelling.

Without it:

- The building may be technically illegal

- Renovations become harder to license

- Banks may refuse mortgages

- Future resale becomes more complicated

What changed under Simplex

Since 2024:

- The notary no longer requires the licence to complete the deed

- The buyer can waive the requirement

- The sale proceeds normally

But critically:

Waiving the licence does not legalise the building.

It only means the buyer is knowingly accepting any future licensing risk.

Why this matters more than it seems

Many properties in Portugal fall into one of these categories:

- Built before 1951 with no formal licence

- Extended later without approval

- Partially licensed but modified over time

- Annexes, garages, pools built informally

Under the old system, these issues had to be resolved before sale.

Under the new system, they can be postponed — and inherited by the buyer.

Banks have not embraced Simplex

This is the key practical nuance.

Even though the law allows sales without licences, most Portuguese banks still:

- Refuse to lend on properties without a valid licence

- Or demand proof that licensing can be regularised

So a property may be:

- Legally sellable

- But not mortgageable

Buyers who sign a CPCV assuming Simplex protects them can discover too late that the bank refuses financing — putting their deposit at risk.

Common real-world scenarios

- A charming pre-1951 house marketed as “no licence required”

- Buyer signs CPCV without financing clause

- Bank refuses mortgage due to missing licence

- Buyer cannot complete

- Deposit is forfeited

Or:

- Property has licensed main house

- Unlicensed annex used as guest suite

- Buyer discovers later that annex must be demolished or legalised at significant cost

When buying without a licence can be reasonable

It is not always a deal-breaker.

Experienced buyers sometimes proceed if:

- Price reflects the risk

- A lawyer confirms exemption eligibility

- An architect confirms likelihood of legalisation

- Cash purchase avoids bank issues

But this is a calculated decision, not something to discover at the notary table.

The essential protection

If a licence issue exists, your CPCV should:

- Clearly state licence status

- Confirm whether exemption applies

- Include right to withdraw if bank rejects financing

- Or require seller to obtain licence before deed

Without this, you accept open-ended liability.

The practical takeaway

Simplex made sales faster.

It did not make illegal buildings legal.

It simply changed who carries the risk.

Next, we’ll move away from paperwork and law, and into something more tangible:

What Portuguese buildings are actually like to live in — especially in winter — and why surveys matter far more here than most foreign buyers expect.

Surveys, Construction Quality, and the Winter Reality

Portugal sells itself on sun, beaches, and outdoor living.

And in summer, many Portuguese homes feel perfect.

But winter is when the real character of a building reveals itself — and it’s also when most foreign buyers realise they didn’t fully understand what they were buying.

Surveys are not culturally standard

In the UK, a building survey is routine.

In the US, home inspections are expected.

In Portugal, many local buyers skip them entirely.

Estate agents don’t push them.

Notaries don’t require them.

Lawyers don’t inspect buildings.

So unless you commission a survey, nobody else is checking the structure for you.

That single fact explains many of the “nightmare renovation” stories you see in expat forums.

Typical structural realities

Common issues found in older Portuguese properties:

- No wall insulation

- Single-glazed aluminium windows

- Unsealed roof tiles

- No cavity walls

- Missing damp barriers

- Poor drainage around foundations

These aren’t necessarily “defects” by Portuguese construction standards — they are simply how houses were built for decades in a warm climate.

The winter shock

Foreign buyers often view properties in:

- Spring sunshine

- Summer heat

- Dry weather

Then winter arrives:

- Indoor humidity rises

- Walls feel cold and damp

- Condensation forms on windows

- Mold appears behind furniture

- Electric heaters run constantly

Many Portuguese homes are effectively designed to stay cool in summer — not warm in winter.

The result:

- Higher heating costs than expected

- Ongoing mold remediation

- Need for insulation retrofits

Bubbling paint is not cosmetic

A classic Portuguese property viewing moment:

- Agent says: “Just a bit of paint needed”

- Buyer sees bubbling paint

- Assumes minor decoration

In reality, bubbling paint often indicates:

- Rising damp

- Water ingress through walls

- Roof leakage

- Failed external render

Fixing paint costs €200. Fixing the cause can cost €5,000–€20,000+.

Roofs deserve special attention

Traditional tiled roofs:

- Often lack modern underlay membranes

- May have broken or slipped tiles

- Allow wind-driven rain infiltration

- Have no insulation layer

A roof replacement or upgrade can easily run into five figures — and scaffolding costs alone can surprise foreign buyers.

Old stone houses: beautiful but complex

Stone properties in rural areas are charming, but:

- Have no damp proof courses

- Absorb moisture naturally

- Require breathable lime-based materials

- Cannot be treated like modern brick construction

Renovating them incorrectly (e.g. cement renders, modern paints) can worsen damp problems.

This is specialist work — not general builder territory.

Seismic standards

Buildings constructed before the 1980s generally:

- Do not meet modern earthquake resistance standards

- Especially in historic city centres

Most of the time this is not an active concern — but it affects:

- Insurance

- Mortgage risk models

- Renovation planning

What a good survey in Portugal should include

A proper surveyor should check:

- Roof structure and water ingress

- Wall moisture readings

- Window glazing type

- Drainage and ground levels

- Electrical system age and safety

- Plumbing condition

- Signs of structural movement

Cost: typically €300–€800.

Potential savings: tens of thousands.

The practical takeaway

In Portugal:

A legal house can still be a damp, cold, expensive surprise.

A survey isn’t about perfection — it’s about knowing:

- What you’re buying

- What it will cost to improve

- Whether the price reflects reality

Next, we’ll look at something buyers only discover after purchase:

Condominium fees, building management, and surprise repair bills — and how to spot them before you buy.

Condominiums, Building Management, and Surprise Costs

If you’re buying an apartment or condo in Portugal, you’re not always just buying an apartment.

You’re buying into a condominium — and that condominium may be well-run, underfunded, chaotic, or quietly sitting on major upcoming repair bills.

This is one of the least understood parts of Portuguese property ownership for foreign buyers, and one of the easiest places to inherit unexpected costs.

What a condominium actually is

A condominium (condomínio) is the legal structure governing shared buildings. It covers:

- Stairwells and corridors

- Roof and exterior walls

- Elevators

- Shared gardens or pools

- Building insurance

- Common-area electricity and water

Every owner pays a monthly or quarterly fee (quota de condomínio) based on their proportional share (permilagem).

Typical fee ranges

Very roughly:

- Small old buildings: €30–€80/month

- Mid-size city buildings with elevator: €80–€150/month

- New developments with pools, gardens, security: €150–€400+/month

But the real issue is not the regular fee.

It’s the irregular ones.

Extraordinary fees: the real surprise

When a building needs major work:

- Roof replacement

- Exterior facade repair

- Elevator overhaul

- Structural reinforcement

- Plumbing riser replacement

The condominium issues an extraordinary levy (quota extraordinária).

This can be:

- €2,000

- €5,000

- €10,000+ per apartment

And it is legally binding on whoever owns the property at the time the decision was made — which might be you, even if the problem existed before you bought.

Why this catches foreign buyers

Because many buyers:

- Ask only “What is the monthly fee?”

- Don’t ask for meeting minutes

- Don’t ask about reserve funds

- Don’t ask about planned works

Portuguese sellers rarely volunteer this information unless asked.

The document you must request: the Atas

Condominium meeting minutes are called atas.

These reveal:

- Complaints about leaks or structural issues

- Discussions of planned repairs

- Votes on upcoming extraordinary fees

- Disputes between owners

- Unpaid fee arrears in the building

Reading the last 2–3 years of atas is one of the simplest ways to spot a future €10,000 surprise before you buy.

Reserve funds: often insufficient

Many older buildings have:

- Minimal reserve funds

- No long-term maintenance planning

- Deferred repairs

This is cultural, not malicious — but it means repair bills eventually land on current owners.

Building administrators vary widely

Some buildings have:

- Professional management companies

- Proper accounts

- Planned maintenance

Others have:

- A volunteer neighbour as administrator

- Informal record-keeping

- Poor debt collection

- Conflict between owners

A dysfunctional condominium can make even a nice apartment stressful to own.

Insurance is part of the puzzle

Building insurance is mandatory, but:

- Older buildings cost more to insure

- Past claims raise premiums

- Some buildings underinsure to reduce fees

If a major incident occurs, underinsurance can mean further levies.

The practical takeaway

When buying an apartment in Portugal, your due diligence checklist must include:

- Current condominium fee

- Reserve fund balance

- Last 2–3 years of atas

- Any planned major works

- Confirmation of no unpaid fees

If your lawyer doesn’t request these automatically, ask them to.

Next, we’ll move to a part of the buying process that feels modern and digital — but is surprisingly opaque:

Property listings, estate agents, and how the Portuguese search market really works.

Property Listings, Agents, and the Search Reality

Most buyers begin their Portuguese property search online.

Idealista.

Imovirtual.

Casa Sapo.

Facebook groups.

WhatsApp messages forwarded by agents.

It looks modern, searchable, and data-rich.

In reality, the Portuguese listing ecosystem is fragmented, opaque, and lightly regulated — and understanding how it works gives you an immediate advantage.

No MLS means no single source of truth

Unlike the US, Portugal has:

- No central Multiple Listing Service (MLS)

- No shared database of active listings

- No public record of final sale prices

Each agency controls its own listings. Platforms simply aggregate what agents upload.

The result:

- Duplicate listings everywhere

- Different prices for the same property

- Outdated listings that sold months ago

- Listings that were never actually available

Most importantly: it’s very hard to know how much a property is worth. You can’t easily see what the property was bought for and what neighboring properties sold for.

Bait listings are common

A well-known industry tactic:

- Attractive property

- Excellent photos

- Unrealistically good price

But:

- Already sold

- Never existed

- Or deliberately mispriced

Purpose: generate leads so agents can offer you “similar alternatives”.

Not fraud in the criminal sense — but a frustrating reality for buyers.

Agents work for sellers, not buyers

By law and custom:

- The agent is paid by the seller

- Typically ~5% + VAT commission

- Their duty is to the seller’s interests

Many foreign buyers subconsciously assume agents “help both sides”. In practice, their incentive is:

- Higher price

- Faster sale

- Listings where they hold exclusive contracts

This doesn’t mean agents are dishonest — but their incentives are not aligned with yours.

Buyer’s agents exist, but are rare

A small but growing niche:

- Independent buyer’s agents

- Paid directly by the buyer

- Help source off-market deals

- Coordinate viewings

- Filter legal risks early

Useful for time-poor foreign buyers — but not yet mainstream in Portugal.

Negotiation culture is flexible

Asking prices in Portugal are:

- Often optimistic

- Especially for older properties

- Especially targeting foreign buyers

Discounts of:

- 10–20% are common

- More if property needs work

- Less in prime urban areas

But without transparent sold-price data, pricing is as much art as science.

Next, we’ll look at rural and land purchases — where the risks and quirks become even more uniquely Portuguese: Rustic vs urban land, water rights, boreholes, and septic systems.

Rural Properties, Land Classification, and Water Rights

If apartments in cities come with condominium surprises, rural properties come with something even more fundamental:

Land in Portugal is not automatically buildable — even if a house is already standing on it.

This catches more foreign buyers off guard than almost any other issue.

Urban vs. Rustic land: the classification trap

Every plot of land in Portugal is legally classified as either:

- Terreno Urbano — urban land (buildable, extendable, developable with permits)

- Terreno Rústico — rustic land (agricultural or protected; building highly restricted)

Here’s the nuance:

A property can contain both.

A very common situation:

- The house footprint is classified as urban

- The surrounding land is classified as rustic

So you buy:

- A legal house

- On a large plot

- But cannot legally extend, add a pool, build a guesthouse, or add garages on most of the land

Many buyers only discover this after purchase — usually when they submit renovation plans and the municipality rejects them.

Reclassifying rustic land is rarely simple

Changing land from rustic to urban:

- Requires municipal planning approval

- Must align with regional zoning plans

- Can take years

- May be impossible if land falls under:

- RAN (protected agricultural reserve)

- REN (ecological reserve)

If land is under RAN or REN, development is usually forbidden outright.

Illegal rural extensions are common

Because of these restrictions, many rural properties have:

- Guest annexes

- Extra bedrooms

- Garages

- Pools

…built informally without licences.

They may exist physically.

They may have existed for years.

But they may be:

- Unlicensed

- Uninsurable

- Unmortgageable

- Subject to demolition orders

Water: the hidden rural deal-breaker

Many rural properties are not connected to mains water.

Instead they rely on:

- Wells (poços)

- Boreholes (furos)

- Rainwater tanks

The critical nuance:

Boreholes must be licensed with the Agência Portuguesa do Ambiente (APA).

But many older boreholes:

- Were drilled decades ago

- Were never registered

- Are technically illegal

If discovered:

- The APA can issue fines

- Order the borehole sealed

- Leave the property with no legal water source

Water extraction tax

Some boreholes are also subject to:

- TRH (water resources tax)

- Annual fees based on extraction volume

Many owners don’t realise this liability exists until after purchase.

Septic tanks: another licensing layer

If the property is not connected to mains sewage:

- It must have a licensed septic system (fossa)

But older septic tanks may be:

- Undersized

- Unlicensed

- Failing environmental standards

Replacing or legalising a septic system can cost:

- €5,000–€20,000+

- And requires municipal and environmental approvals

Utilities depend on water legality

Another very Portuguese quirk:

- You cannot obtain or reconnect electricity

- Without proving legal water and sewage compliance

So a property can look fully habitable — yet sit in bureaucratic limbo because its borehole or septic tank is not properly licensed.

Rural inheritance tangles

Rural properties are also where inheritance issues concentrate:

- Houses passed through generations

- Multiple heirs across countries

- Missing paperwork

- Undivided ownership shares

It is not unusual for a rural ruin to have:

- 10–20 legal heirs

- Some unknown or unreachable

Without every heir signing, the sale cannot legally complete — even if one family member claims to be “the owner”.

The practical takeaway

Rural Portuguese properties are often:

- Beautiful

- Good value

- Full of potential

But they require more legal and technical due diligence than urban properties.

Before signing anything on a rural purchase, your team should verify:

- Urban vs rustic classification

- RAN / REN restrictions

- Building licence status

- Borehole licence

- Septic licence

- Utility feasibility

- Full ownership chain

Skipping any one of these is how dream quintas become multi-year legal projects.

Timelines, Bureaucracy, and the Reality of “Portuguese Time”

Foreign buyers often ask:

“How long does it take to buy a property in Portugal?”

The honest answer:

Longer than you expect. And rarely on the schedule you were promised.

This isn’t incompetence. It’s simply how Portuguese administrative culture operates — and understanding this saves stress, money, and failed deals.

The theoretical timeline

On paper, a clean purchase looks like this:

- Offer accepted

- Due diligence: 2–4 weeks

- CPCV signed

- Mortgage approval: 4–8 weeks

- Escritura scheduled

- Completion

Total: 8–12 weeks

And occasionally — especially for cash buyers in modern urban apartments — this really happens.

The lived reality

In practice, timelines stretch because:

- Documents are missing

- Registries need corrections

- Municipal records don’t match reality

- Bank valuation takes longer

- Someone goes on holiday

- A signature is delayed

- A notary has no available slots

Suddenly:

- 3 months becomes 6

- 6 becomes 9

- Complex rural or renovation purchases can exceed a year

“Next week” rarely means next week

A uniquely Portuguese cultural nuance:

Directly saying “no” is considered impolite.

So you’ll often hear:

- “Sim, sim, para a semana.”

- “I’ll send it tomorrow.”

- “No problem, we’ll handle that.”

But what they often mean is:

- “I’m busy”

- “This isn’t urgent to me”

- “I don’t want to say no”

Experienced buyers learn a simple rule:

If something matters, follow up repeatedly. Politely.

Silence rarely means progress.

August: the national pause button

Portugal effectively slows down in August.

- Lawyers take holidays

- Notaries reduce hours

- Municipal engineers disappear

- Builders close sites

- Banks run skeleton staff

Trying to:

- Close an escritura

- Get renovation approval

- Obtain missing licences

…in August is usually futile.

Plan timelines assuming:

- Nothing critical happens in August

- Expect 3–5 week dead time mid-summer

Municipal timelines vary wildly

Câmara Municipal efficiency depends entirely on:

- Which town

- Which department

- Which person handles your file

One council may issue a licence in 30 days.

Another may take 9 months for the same request.

There is no reliable national standard — despite official statutory deadlines.

Mortgage timing vs CPCV deadlines

This is where most failed deals happen.

Banks:

- Take longer than expected

- Ask for additional documents late

- Schedule valuations slowly

- Re-run risk checks

Meanwhile your CPCV:

- Has a fixed completion deadline

- With deposit at risk

If your mortgage isn’t finalised in time:

- You must renegotiate an extension

- Or risk losing your deposit

This is why financing-contingency clauses are so important — and why sellers resist them in hot markets.

Notary bottlenecks

Notaries are:

- Public officials

- Appointments-only

- Often fully booked weeks ahead

Even when everything is ready:

- You may wait 2–4 weeks for an escritura slot

Utility and registration lag after completion

After purchase:

- Land Registry updates can take months

- Tax records update later still

- Utility transfers can stall without notarised deed copies

- Internet installation may need new infrastructure approval

You legally own the property — but administratively, the system takes time to recognise it.

The psychological adjustment

Buying property in Portugal requires:

- Patience

- Redundancy in timelines

- Low emotional attachment until completion

- Buffer accommodation plans

- Buffer budgets

Buyers who approach Portugal expecting:

- UK-style fixed schedules

- Automated processes

- Immediate responses

are the ones who feel something is “wrong”.

In reality:

This is simply the operating system.

The practical takeaway

Plan every timeline with:

- Extra months, not weeks

- Holiday shutdowns

- Document delays

- Bank slowdowns

- Notary queues

If it finishes sooner — great.

If not — you’re prepared.

How to Buy Property in Portugal Safely: A Practical Checklist

By now, one thing should be clear: Buying property in Portugal isn’t difficult — but it is unforgiving if you skip steps.

The legal system works. Ownership rights are strong. Foreign buyers are fully protected if they follow the process correctly.

Most horror stories come from:

- Relying on agents instead of lawyers

- Skipping surveys

- Signing contracts too early

- Assuming “it works like at home”

Here’s the condensed roadmap that keeps buyers out of trouble.

Before you make an offer

- Obtain a Portuguese NIF (tax number)

- Open a Portuguese bank account (helps with taxes and utilities)

- Hire an independent lawyer (not the agent’s recommended lawyer)

- Ask for the Certidão Permanente (Land Registry)

- Ask for the Caderneta Predial (Tax Registry)

- Ask whether a Licença de Utilização (habitation licence) exists or is exempt

- Verify urban vs rustic land classification

- If rural: verify water source licences and septic compliance

- Commission an independent property survey

If any document is missing, inconsistent, or “will be ready soon” — pause.

When negotiating

- Treat asking prices as expectations, not facts

- Be cautious with “too good to be true” listings

- Confirm the agent holds a valid AMI licence

- Keep key agreements in email, not only WhatsApp

When signing the CPCV

Ensure your lawyer includes:

- Mortgage approval contingency

- Bank valuation contingency

- Survey contingency (if inspection occurs after signing)

- Clear deadline extensions if delays occur

- Clause requiring delivery free of debts and encumbrances

- Agreement on who pays taxes and fees

- Optional registration of CPCV with Land Registry for added protection

Never sign a CPCV:

- Without completed due diligence

- Without understanding deposit risk

- Without financing clarity

Before the final deed (escritura)

- Confirm mortgage is fully approved

- Confirm IMT and stamp duty funds are ready

- Arrange currency transfers early

- Obtain notarised deed copies immediately after signing

- Confirm notary appointment in advance

After completion

- Initiate Land Registry update

- Transfer utilities

- Register with local municipality

- Verify IMI records update correctly

- If condominium: introduce yourself to the administrator and review accounts

Timeline mindset

- Assume delays

- Avoid August for critical steps

- Keep accommodation flexible

- Don’t book moving trucks until the deed is signed

Final Thoughts: Portugal Rewards the Prepared Buyer

Portugal remains one of Europe’s most appealing places to buy property. Ownership rights are strong, foreigners face no legal restrictions, and demand for well-located homes continues to hold up. For many buyers, the reward is not just an asset, but a lifestyle — sun, space, safety, and a slower pace of life.

What catches people out is not the legality of the system, but its operating style. Portugal is paper-driven rather than digital. It runs on personal relationships more than automated portals. Timelines are flexible rather than fixed. And contracts, once signed, carry real weight. None of this is inherently bad — it is simply different from the UK or US model — but it punishes anyone who assumes the process works the same way as at home.

The buyers who come away happy are rarely the ones who rushed. They assembled the right professionals early, insisted on proper legal and technical checks, allowed extra time for everything, and treated the CPCV with the seriousness it deserves. They viewed delays as normal, not as red flags. And they understood that in Portugal, diligence is not optional — it is the price of entry.

Approach the market on its own terms and the process becomes predictable rather than perilous. Do that, and buying property in Portugal becomes what it was meant to be: a step toward a better life, not a crash course in property law.

Comments are closed.